Cross-Border Wealth Management: Why Your Financial Advisor is Wrong About Expat Money

Most advisors operate within a single-country framework and miss the tax traps, currency mismatches, and structural risks that destroy expat wealth. Your life spans multiple jurisdictions, so traditional advice built for stationary clients creates blind spots.

This piece exposes the hidden commission conflicts, multi-jurisdiction tax problems, and regional wealth traps your advisor won't discuss. You'll find how to build a global wealth management framework that protects your assets across borders.

Why Traditional Financial Advisors Fail Expats

Most financial advisors build their careers managing wealth within a single tax jurisdiction. Their training, licensing, and daily practice revolve around domestic equities, local pension schemes, and home-country tax codes. This approach is effective for clients who remain in one place. Expats face a mismatch between the advisor's expertise and their reality.

The Domestic Portfolio Assumption

Traditional wealth management education teaches advisors to optimise portfolios based on a single country's tax structure, regulatory environment, and currency. They learn to maximize ISA contributions in the UK, recommend 401(k) strategies in the US, or structure superannuation in Australia. The entire framework assumes geographic permanence.

You need something different. A global balance sheet behaves in an entirely different way from a domestic one. Conventional strategies break down when you hold assets in multiple jurisdictions. An advisor trained in London might understand UK inheritance tax but miss how Spanish tax residency triggers wealth tax exposure. A Singapore-based advisor who optimises for local regulations won't anticipate the reporting nightmares you'll face after moving to Brazil.

The problem goes deeper than knowledge gaps. Most advisors operate as product distributors rather than cross-border strategists. They sell what they're licensed to sell, what their institution offers, or what generates the highest commission. Because of these factors, they push solutions designed for stationary clients onto mobile professionals whose circumstances need fluid, jurisdiction-agnostic structures.

Cross-Border Complexity They Miss

Managing wealth in multiple countries is an intricate game of regulatory chess. Every geographic move alters your tax status, inheritance exposure, reporting obligations, and asset protection framework. Your advisor needs to anticipate these changes. Most don't.

Traditional advisors miss how each jurisdiction interacts with the others. They don't track double taxation exposure. They overlook conflicting reporting requirements that can trigger penalties in multiple countries at once. They also don't understand how holding certain investment structures in one country creates tax liabilities in another, and these gaps matter.

Multi-jurisdictional reporting mandates increase the risk of penalties. Brazilian tax authorities maintain some of the most aggressive reporting requirements in the hemisphere. Holding uncoordinated offshore accounts as a Brazilian expat invites severe penalties and administrative gridlock. Your domestic advisor won't flag this risk because they are monitoring Brazilian compliance standards.

Asset protection adds another layer of complexity. Assets held in the GCC can be frozen instantly upon your passing without formal offshore structuring. Your international family then faces local sharia-compliant distribution laws, whatever their nationality. Traditional advisors rarely address these probate realities because they fall outside their standard service model.

Geographic Mobility Changes Everything

Your geographic location might change every three to five years. You might earn in UAE dirhams, spend in euros, and maintain long-term liabilities in British pounds or Singapore dollars. This multi-currency reality needs asset-liability matching that traditional advisors ignore.

Advisors recommend rigid, illiquid structures that lock up capital for 10, 15, or 20 years. These products carry hidden exit penalties and complex contractual terms. These structures are counterproductive for someone whose circumstances change regularly. You need liquidity and flexibility. Your advisor sells products designed for retirees who will age in place.

The misalignment extends to currency risk management. Traditional advisors might vary holdings by asset class but rarely match your assets to your future expenses in different currencies. Failing to match assets with future liabilities kills purchasing power silently. You watch your wealth erode not through poor investment selection but through currency mismatches your advisor never addressed.

Cross-border wealth management requires specialised expertise that most traditional advisors simply lack. Their domestic training creates blind spots that cost you money, expose you to unnecessary risk, and leave your wealth vulnerable on multiple fronts.

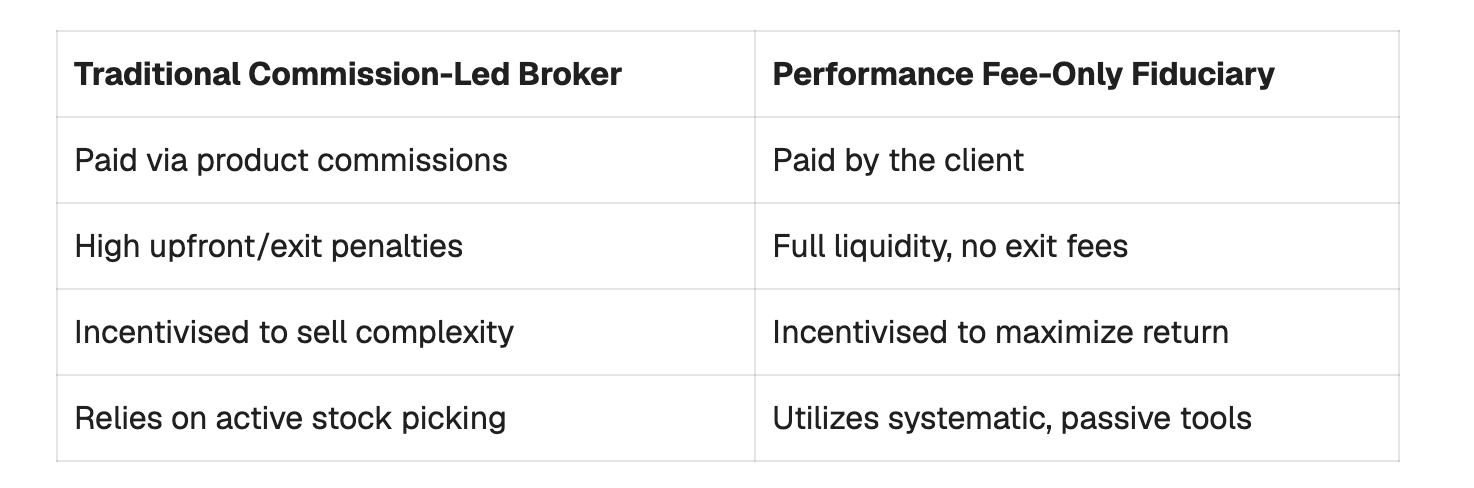

The Commission Model: Your Advisor's Hidden Conflict

The single greatest systemic risk to expat wealth is not market volatility but a fundamental misunderstanding of advisor incentives. A staggering percentage of international financial advisors do not operate under a true fiduciary mandate. They operate as product distributors whose compensation structure creates unavoidable conflicts of interest.

How Product Commissions Work

The advisor's compensation is derived from upfront or trailing commissions paid by product providers. Their allegiance is to the financial institution, not you. This payment structure explains why certain investment products appear in expat portfolios despite being unsuitable for mobile professionals.

The advisor receives a commission each time they place your capital into a specific product. The higher the internal fees embedded in the product, the larger the commission paid to the advisor. So you see persistent recommendations for products with high embedded costs and complex contractual terms. The advisor profits from placement, whatever the product does for your cross-border needs.

Exit Penalties and Lock-In Periods

The commission model creates another problem: illiquidity. These products lock up capital for 10, 15, or 20 years. Hidden exit penalties make early withdrawal prohibitively expensive. For an expat whose geographic location might change every three to five years, these rigid, illiquid structures are counterproductive.

You just need flexibility. Tax residency changes trigger restructuring needs. Currency shifts require portfolio rebalancing. New reporting obligations ask for account consolidation. Locked capital prevents you from adapting to these realities. You either pay severe penalties to exit or remain trapped in unsuitable structures as your circumstances evolve.

Performance Fee vs. Commission Models

Sophisticated global investors reject commission-based models in favour of a true performance fee-only fiduciary framework. Under this model, the wealth manager's incentives arrange with your balance sheet. The fiduciary advisor does not profit if the portfolio does not grow.

This eliminates the incentive to generate high transaction volumes or recommend complex investment products. It prioritises cost minimisation, absolute fee transparency, and long-term capital compounding.

The difference matters in cross-border wealth management. Commission structures push products designed for stationary clients onto mobile professionals. Performance fee structures arrange advisor success with your actual wealth growth. The payment model determines whether your advisor acts as a salesman or a fiduciary partner.

The Multi-Jurisdiction Tax Problem

Beyond advisor conflicts lies a structural problem that no commission-free relationship can solve on its own: the multi-jurisdiction tax web. Each country maintains its definition of tax residency, its reporting standards and its own claim on your income. These systems collide and erode wealth silently and systematically once you cross borders.

Tax Residency Rules Keep Changing

Tax residency doesn't follow a universal standard. Each jurisdiction applies different criteria to determine whether you owe taxes on worldwide income. Some countries count physical presence days. Others may consider the location of your "permanent home" or "centre of vital interests". A few claim tax residency based on citizenship alone, whatever your place of residence.

Portugal's Non-Habitual Resident (NHR) framework undergoes ongoing structural modifications. You need careful management of foreign-sourced income, dividend distributions and the precise timing of asset liquidations. Most advisors lack the attention to detail that navigating this evolving tax-friendly landscape demands.

Spain presents a complex dual reality. The "Beckham Law" offers an attractive flat tax rate for inbound executives and digital nomads. Those sitting outside its scope face an aggressive progressive tax system and a controversial wealth tax (Impuesto sobre el Patrimonio). You can suffer severe capital erosion if you fail to structure assets via compliant cross-border wrappers before establishing Spanish tax residency.

Italy's aggressive play for the global elite features an attractive lump-sum flat tax regime for new residents. You can substitute all foreign-sourced income taxes with a fixed annual fee. Accessing and maintaining this status requires multi-jurisdictional reporting and clarity on the legal definition of "foreign-sourced" wealth.

The problem intensifies once residency rules change mid-year or you maintain ties to multiple countries at once. You might trigger tax residency in two jurisdictions at the same time, with both countries claiming the right to tax your global income.

Double Taxation Exposure

Conflicting residency claims make double taxation a ground threat rather than a theoretical concern. Tax treaties exist to prevent this scenario, but they operate imperfectly. Treaty relief requires proper documentation, timely filing and knowledge of which treaty provisions apply to specific income types.

Your investment income might face withholding tax in the source country and then get taxed again in your country of residence. Capital gains on property sales can trigger liability in both the property's location and your tax home. Pension distributions often create multi-jurisdictional tax obligations that advisors miss entirely.

Wealth taxes operate independently of income taxes. Spain's wealth tax applies to your global assets once you establish tax residency, whatever the location of those assets or whether they generate income. Other jurisdictions impose estate taxes, inheritance taxes or gift taxes that stack on top of income obligations.

Reporting Requirements Across Borders

The administrative burden of multi-jurisdiction wealth extends beyond tax liability into reporting mandates. Each country where you hold accounts, earn income or maintain assets demands disclosure. Missing these requirements triggers penalties that compound quickly.

Brazil represents a challenging fiscal environment. The Brazilian tax authority (Receita Federal) maintains some of the most aggressive and complex reporting requirements in the hemisphere. Recent global changes targeting offshore wealth mean that historic structures like offshore trusts and traditional private investment companies face intense regulatory scrutiny and tax transparency mandates that are constantly changing.

A Brazilian expat or an international investor with Brazilian exposure who holds uncoordinated offshore accounts invites severe penalties, double taxation and administrative gridlock. The reporting standards don't just require disclosure of account balances. They demand detailed transaction reporting, currency conversion documentation and proof of tax payment in foreign jurisdictions.

Your advisor won't track these multi-jurisdictional reporting deadlines because they operate within a single regulatory framework. Missing a filing in one country can trigger automatic information exchange protocols that create problems in another jurisdiction entirely.

Regional Wealth Traps Your Advisor Won't Tell You About

Each expat destination carries location-specific wealth traps that surpass general tax complexity. Local regulatory frameworks, cultural financial practices, and market structures create these regional pitfalls that domestic advisors rarely understand. The financial decisions you make in one jurisdiction create consequences that only demonstrate themselves when you relocate or attempt to access your capital years later.

GCC Region: Commission Heaven and Probate Nightmares

The Gulf Cooperation Council region remains one of the world's most powerful engines for wealth accumulation. The UAE cements its status as a global financial hub amid massive economic transformations in Saudi Arabia and the institutional stability of Qatar. The region offers exceptional tax-optimised liquidity.

But the GCC is also the global centre for predatory financial salesmanship. These jurisdictions operated outside rigid Western regulatory frameworks, so they became a haven for commission-driven brokers. Expats in Dubai, Doha, and Riyadh get locked into opaque, multi-decade contractual savings plans or pitched high-yield property loan notes that carry unhedged structural risks routinely.

Many expats overlook local probate realities. Assets held within the GCC can be frozen upon your passing without formal offshore structuring or DIFC/ADGM wills. This subjects international families to local sharia-compliant distribution laws, whatever their nationality. Your UK passport doesn't protect your estate from local inheritance procedures.

Southern Europe: Wealth Taxes and Beckham Law Misunderstandings

Southern Europe has undergone a structural renaissance and transformed into a primary destination for location-independent professionals and digital entrepreneurs. Specialised tax incentives, which are designed to attract global capital, are driving this change.

Spain presents a complex dual reality. The "Beckham Law" offers an attractive flat tax rate for inbound executives and digital nomads, but those sitting outside its scope face an aggressive progressive tax system and a controversial wealth tax (Impuesto sobre el Patrimonio). Failing to structure assets via compliant cross-border wrappers before establishing Spanish tax residency can result in severe capital erosion.

Portugal maintains its status as a premier European destination despite ongoing structural modifications to its Non-Habitual Resident framework. Careful management of foreign-sourced income, dividend distributions, and the precise timing of asset liquidations is what you need to navigate this evolving landscape.

Italy's aggressive play for the global elite features an attractive lump-sum flat tax regime for new residents. You can substitute all foreign-sourced income taxes with a fixed annual fee. But accessing and maintaining this status requires meticulous multi-jurisdictional reporting and absolute clarity on the legal definition of "foreign-sourced" wealth.

Singapore: Institutional Fee Layering

Singapore attracts wealth through its rock-solid legal framework, absolute political stability, and robust single-family office structures. Yet the trap in Singapore is usually not regulatory malfeasance. Rather, it is the quiet erosion of wealth through institutional overlayering that occurs.

Private banks pile on fees upon fees. They charge management fees, transaction costs, and underlying product expenses that drag down net performance quietly. Malaysia serves as a critical strategic corridor through the Labuan International Business and Financial Centre, offering sophisticated mid-shore corporate structuring.

Brazil: Offshore Structure Penalties

Brazil represents a challenging fiscal environment. The Brazilian tax authority (Receita Federal) maintains some of the most aggressive and complex reporting requirements in the hemisphere. Recent global changes targeting offshore wealth mean historic structures like offshore trusts and traditional private investment companies face intense regulatory scrutiny.

For a Brazilian expat or an international investor with Brazilian exposure, holding uncoordinated offshore accounts can lead to severe penalties, double taxation, and administrative gridlock. The reporting standards don't just demand account balances but detailed transaction reporting across all foreign holdings.

Currency Risk and Asset-Liability Mismatch

Currency exposure stands at the heart of every cross-border wealth management decision, yet most advisors treat it as an afterthought. Your lifestyle operates in multiple monetary systems at once and creates mismatches between where you earn, where you spend, and where your liabilities exist. This disconnect erodes purchasing power silently, whatever the performance of your investments.

The Multi-Currency Lifestyle Reality

Expats face multi-currency lifestyles by nature. You might earn in UAE dirhams (pegged to the USD), maintain lifestyle expenses in euros (Spain/Portugal), and hold long-term liabilities in British pounds or Singapore dollars. Each currency fluctuates on its own and creates exposure that compounds over time.

Your income, expenses, and assets operate in different currencies. Exchange rate movements affect your real-life wealth directly. A strong dollar might boost your earning power in Dubai, but euro weakness erodes your future purchasing power if your retirement property sits in Portugal and you plan to retire there. Your investment portfolio might show gains in nominal terms while losing ground in the currency that matters for your actual spending.

Traditional advisors miss this reality because they optimise portfolios with a single base currency. They track performance in dollars or pounds without thinking over whether those are the currencies you'll actually use. You accumulate wealth in currencies disconnected from your future needs as a consequence.

Matching Assets to Future Expenses

Your purchasing power dies a silent death when you fail to match assets with future liabilities. Your investment strategy must line up with the currency denomination of your actual future expenses. Your portfolio needs euro-denominated exposure if you plan to retire in Spain. You need Singapore dollar stability if your children's education costs arise in Singapore.

Most expat portfolios ignore this principle. They chase returns without thinking over currency risk. You might hold a portfolio heavily weighted toward US equities because American markets outperformed in the recent past. But dollar volatility creates uncertainty that undermines your financial planning if your expenses occur in euros or pounds.

Why Currency Hedging Gets Ignored

Cross-border wealth management requires explicit currency strategy, yet advisors overlook hedging mechanisms. The reason is structural. Most advisors lack the technical expertise to implement multi-currency hedging strategies. They understand domestic asset allocation but don't grasp how to build portfolios that hedge specific currency exposures while maintaining growth potential.

Currency hedging adds complexity that reduces commission opportunities similarly. Simple, transparent currency-matched portfolios using passive instruments generate lower fees than complex structured products. Your advisor profits more from selling high-fee guaranteed products than from building disciplined currency hedging strategies.

The oversight creates real consequences. Your portfolio becomes a speculative bet on exchange rate movements you never intended to make without intentional currency matching. Your wealth grows or shrinks based on monetary policy decisions in countries where you don't live and affects currencies you don't spend.

Portfolio Fragmentation Destroys Wealth

Many HNWIs mistakenly equate a complex portfolio with a sophisticated one. Accumulation becomes the strategy. You build wealth in stages across different countries, opening accounts wherever it seems convenient at the time. A broking account in Singapore. A property portfolio in Spain. A legacy pension in the UK. Private equity exposure in the UAE. Each piece makes sense in isolation. Together, they create chaos.

The Uncoordinated Account Problem

This fragmentation creates a profound lack of visibility. You can't see your true global asset allocation when holdings scatter across institutions, jurisdictions, and currencies. You remain blind to your combined currency risk, concentration risks, and hidden structural costs.

The problem compounds because each account operates independently. Your Singapore broker recommends growth stocks. Your Spanish property manager suggests more real estate. Your UK pension administrator adjusts nothing. None of these parties communicate. None possess a complete picture of your wealth. You might hold overlapping exposures across accounts while believing you've diversified.

Hidden Concentration Risks

Fragmented accounts mask concentration that would be obvious in a united view. You might hold technology stocks in your Singapore broking, own commercial property in Dubai's tech hub, and maintain private equity in digital infrastructure companies. Each account appears diversified within its silo. You've bet your entire wealth on one sector across multiple structures.

Geographic concentration follows the same pattern. Holding property in Portugal, Spanish equities through your EU account, and Italian bonds creates a euro zone concentration that your advisors won't flag. Currency risk analysis requires viewing all holdings together. Fragmentation prevents this visibility.

Counterparty risk multiplies across institutions. You trust multiple banks, brokers, and fund managers without understanding your total exposure to any single financial system failure. Bringing everything together reveals these dependencies.

Fee Duplication Across Accounts

Each account charges its own management fee, custody fee, and transaction costs. Five separate accounts means paying five sets of administrative charges. These costs stack without delivering additional value. You're paying multiple institutions to manage pieces of a puzzle none of them can see completely.

Hidden platform fees compound the problem. Your Singapore account charges 1.2% annually. Your UK pension takes 0.8%. Your UAE structure adds another layer. None of these fees show up on a single statement. Calculating your true all-in cost requires a manual combination that most expats never perform.

DIY Platform Limitations

The rise of online DIY investment platforms has created a dangerous countertrend: the 5-minute retirement plan illusion. Low-cost brokers are excellent execution tools. They offer rock-bottom fees and instant access. But they do not provide cross-border tax advice, estate planning coordination, or structural asset protection.

A well-laid-out, globally united investment strategy beats a collection of uncoordinated accounts every time. DIY platforms excel at execution but fail at strategy. They can't tell you how your holdings interact across tax jurisdictions or whether your estate structure protects heirs in multiple countries.

The 2027 UK Pension Inheritance Tax Shift

The global expat community faces an unprecedented disruption to the regulatory landscape, especially those with historic ties to the UK. The impending 2027 UK pension inheritance tax changes will bring qualifying pension schemes within the scope of UK IHT. This change dismantles one of the most reliable wealth transfer mechanisms available to cross-border families.

What Changes in 2027

International professionals viewed pensions as a bulletproof estate-planning tool that could pass to heirs tax-free for decades. Pension assets sat outside the inheritance tax net and allowed families to transfer accumulated retirement savings across generations without triggering the 40% IHT charge. That safety net will disappear from 2027.

Qualifying pension schemes will fall within the IHT framework. Your pension pot becomes subject to the same inheritance tax rules that apply to other estate assets, whatever the size or how you've built it across jurisdictions. The UK government is closing what it views as a loophole that allowed substantial wealth to escape taxation upon death.

Effect on Cross-Border Families

Cross-border families have disproportionate exposure to this rule change. You might have accumulated pension wealth while working in London and then relocated to Dubai, Singapore or Spain. Your pension remains a UK asset subject to UK inheritance tax rules even though you no longer live in Britain.

You face the real prospect of a 40% tax hit on accumulated retirement savings without proactive restructuring, offshore life insurance policies or specialised wealth wrappers. Your heirs might reside in different countries with their inheritance tax regimes. The 2027 change could trigger double taxation scenarios where both the UK and your country of residence claim portions of the same pension assets.

The geographic complexity intensifies the problem. Advisors operating in your current country of residence may not track UK pension rule changes. UK-based advisors might not understand how the 2027 change interacts with estate planning structures you've established in other jurisdictions.

Restructuring Before the Deadline

This rule change underscores a vital truth: wealth strategies cannot remain static. You have a window to restructure pension assets before the 2027 implementation. Options include moving pension wealth into offshore life insurance wrappers, establishing compliant trust structures or repositioning assets into vehicles that remain outside IHT scope.

The restructuring process requires coordination across jurisdictions. Your UK pension might need to interface with estate planning tools in the GCC, trust structures in Singapore or tax-efficient wrappers available through other jurisdictions. This coordination requires specialised cross-border wealth management expertise that takes into account both current regulations and upcoming changes.

Building a True Cross-Border Wealth Management Framework

Preserving wealth across multiple jurisdictions requires a systematic, institutional approach built on four non-negotiable pillars.

Fiduciary-Only Relationships

Your wealth infrastructure must move away from transactional brokers and commission-based platforms. A relationship with an appointed, regulated fiduciary whose fee structure is transparent and directly tied to your net asset growth forms the foundation of all wealth preservation that works. The advisor does not profit if the portfolio does not grow. This alignment eliminates the incentive to generate high transaction volumes or recommend unnecessarily complex investment products. Instead, cost minimisation and long-term capital compounding are prioritised.

Structural Asset Protection

Resilient asset protection strategies must be in place to withstand cross-border tax friction, changing inheritance tax boundaries, and potential legal overreach. Using international estate planning tools, offshore life insurance wrappers, and multi-jurisdictional trust structures that separate legal ownership from economic benefit will protect your global legacy.

Global Portfolio Consolidation

Fragmented, uncoordinated accounts must be eliminated. Your global portfolio should be consolidated into a centralised reporting framework. This will give complete visibility over your global asset allocation and eliminate overlapping fee layers. Precise execution of your multi-currency strategy across distinct regional holdings becomes possible.

Evidence-Based Passive Strategies

You should reject the noise of active fund management, market timing, and speculative alternative investments. Long-term wealth should be built on systematic, academic frameworks: low-cost passive ETFs, institutional-grade fixed income, secured lending certificates, and highly disciplined asset allocation models that reflect the strategies of the world's most successful family offices.

Schedule a Private Consultation

Partner with Expat Fiduciary to discover how an institutional-grade, performance-fee-only approach can optimise your cross-border wealth strategy. During this confidential strategy call, we will audit your current portfolio for hidden commission structures and assess how your assets are structured against current tax regimes, whether you're utilising Spain's Beckham Law or protecting GCC-based liquidity. We will review your cross-border estate plan against the impending 2027 UK Pension IHT changes.

Structural fragmentation should not compromise decades of wealth accumulation.

Final Thoughts

Cross-border wealth management presents complexity that most advisors cannot handle. Your geographic mobility demands specialised expertise, fiduciary alignment, and institutional-grade portfolio construction that exceeds domestic investment frameworks. The stakes increase as regulatory environments change and tax boundaries evolve across jurisdictions.

The framework outlined here eliminates hidden commission conflicts, combines fragmented holdings, and protects your wealth against multi-jurisdictional exposure.

Visit the Expat Fiduciary Blog to explore our full library of research papers, regulatory updates, and detailed cross-border wealth analyses. Armed with the right structure and aligned advisory partnership, you can preserve purchasing power across currencies while building a legacy that survives border crossings intact.

FAQs

Q1. Why do traditional financial advisors struggle with expat wealth management?

Traditional financial advisors are trained to manage wealth within a single tax jurisdiction and typically optimise portfolios according to one country's tax structure, regulatory environment, and currency. They often miss critical cross-border complexities like shifting tax residency rules, multi-jurisdictional reporting requirements, and currency mismatches that are essential for expats who move between countries regularly.

Q2. What is the main problem with commission-based financial advisors for expats?

Commission-based advisors earn money from product providers rather than clients, creating a conflict of interest. They're incentivised to recommend high-commission products with expensive exit penalties and long lock-in periods, which are particularly unsuitable for expats who need flexibility due to frequent geographic moves and changing tax circumstances.

Q3. How does portfolio fragmentation harm expat wealth?

When expats hold accounts across multiple countries and institutions without coordination, they lose visibility of their true global asset allocation. This fragmentation masks concentration risks, creates fee duplication across accounts, and prevents proper currency risk management. Each advisor only sees part of the picture, leading to overlapping exposures and unnecessary costs.

Q4. What changes to UK pension inheritance tax are coming in 2027?

From 2027, UK pension schemes will fall within the inheritance tax framework, ending their previous exemption. This means pension assets will be subject to the standard 40% inheritance tax charge upon death, significantly impacting cross-border families who accumulated pension wealth in the UK but now live elsewhere.

Q5. What should expats look for in a cross-border wealth manager?

Expats should seek fiduciary-only advisors who charge fees tied directly to portfolio performance rather than product commissions. The ideal advisor offers global portfolio consolidation, understands multi-jurisdiction tax implications, implements proper currency hedging strategies, and uses evidence-based passive investment approaches instead of complex, high-fee structured products.