What Happens When Private Equity Takes Over Your Financial Advisor?

Your financial advisor's recent change in ownership might seem like a routine business matter, but private equity financial advisors operate under different pressures than independent firms. Private equity buying financial advisors has picked up pace faster than ever, reshaping how advisory businesses function and serve clients like you.

These consolidated firms face conflicts between client interests and investor returns, unlike traditional independent practices. What changes when private equity funds buy financial advisor businesses? Understanding these dynamics can help you protect your investments and ensure you're receiving unbiased advice.

This piece gets into how takeovers alter business models and potential conflicts of interest. Financial pressures affect service quality. You should ask your adviser critical questions after any ownership change.

How private equity buying financial advisors changes the business model

From independent firms to consolidator groups

The numbers reveal the scale of consolidation. Authorised advice firms have fallen 15 per cent since 2021, but adviser numbers remain steady. Around half of all advisers now work in firms with more than 50 advisers. Private equity drove approximately 72 per cent of deals during the first half of 2026

These aren't small acquisitions that absorb struggling practices. Large firms are being folded into multi-layered ownership structures where a sovereign wealth fund or US pension scheme sits several steps removed from the clients who receive advice. The adviser you meet hasn't changed, but the chain of accountability has lengthened.

The change from deal volume to proposition control

The nature of private equity buying financial advisors has changed from acquisition speed to operational control. The practice of buying advice firms solely for scale has ended. Acquirers now must prove they can integrate and grow businesses organically.

The focus has shifted to what the industry refers to as proposition control. This means control over the platform, the portfolios, the fund selection and the data used for client decisions. Firms measure success against the value created, which they execute according to the business plan. Note that language is a value created for the business, not for you as the client.

What vertical integration means for clients

Vertical integration changes who profits from your investments at multiple points. 84 per cent of profiled consolidators run their own in-house model portfolio services, and 68 per cent have their fund range. The firm that acquired your adviser's practice sells its own products.

The same group now owns the advice, the platform and the investment product. It captures margin at every stage. Your adviser may possess the same skills and intentions as before the takeover. But the parent company that signs their payroll also profits when it places you in its funds instead of a competitor's products. This creates a structural conflict between what serves your financial outcomes and what serves the consolidator's revenue targets.

Conflicts of interest when private equity funds buying financial advisors' businesses

In-house investment products vs independent options

The ownership chain creates direct financial incentives to favour proprietary products. Your adviser's parent company profits from both the advice fee and the investment product. The question becomes whether recommendations serve your best interests or the consolidator's revenue targets.

How adviser compensation structures change

Some adviser groups offer explicit or implicit incentives to invest in group products or services. This evidence isn't speculation. Worldwide financial regulators found operational conflicts where advisers face pressure to recommend parent-company products instead of independent options that might cost much less or perform far better.

Several advisers, whose firms were acquired by private equity financial advisers, describe feeling steered towards preferred products. They know that a lower-cost alternative would better serve their clients. The bond of trust between adviser and client faces direct pressure. Most clients remain unaware this tension exists.

The gap between active fund performance and cost

The performance record makes these conflicts especially troubling. 97 per cent of global equity funds underperformed their benchmark over the ten years to June 2026. Your adviser steers you toward their parent company's actively managed funds, and history suggests those funds will cost you money rather than generate returns above a low-cost index alternative.

Why your adviser may recommend parent-company products

The pressure also extends beyond bad actors. Private equity funds buying financial advisors' businesses create vertical integration and extract profits at multiple levels. Your adviser may possess similar skills and ethics as before the takeover. The business structure now rewards recommendations that benefit the consolidator first.

Financial pressures behind consolidated advice firms

Some of the sector's biggest players face visible financial strain. These pressures create incentives that may not match your interests as a client.

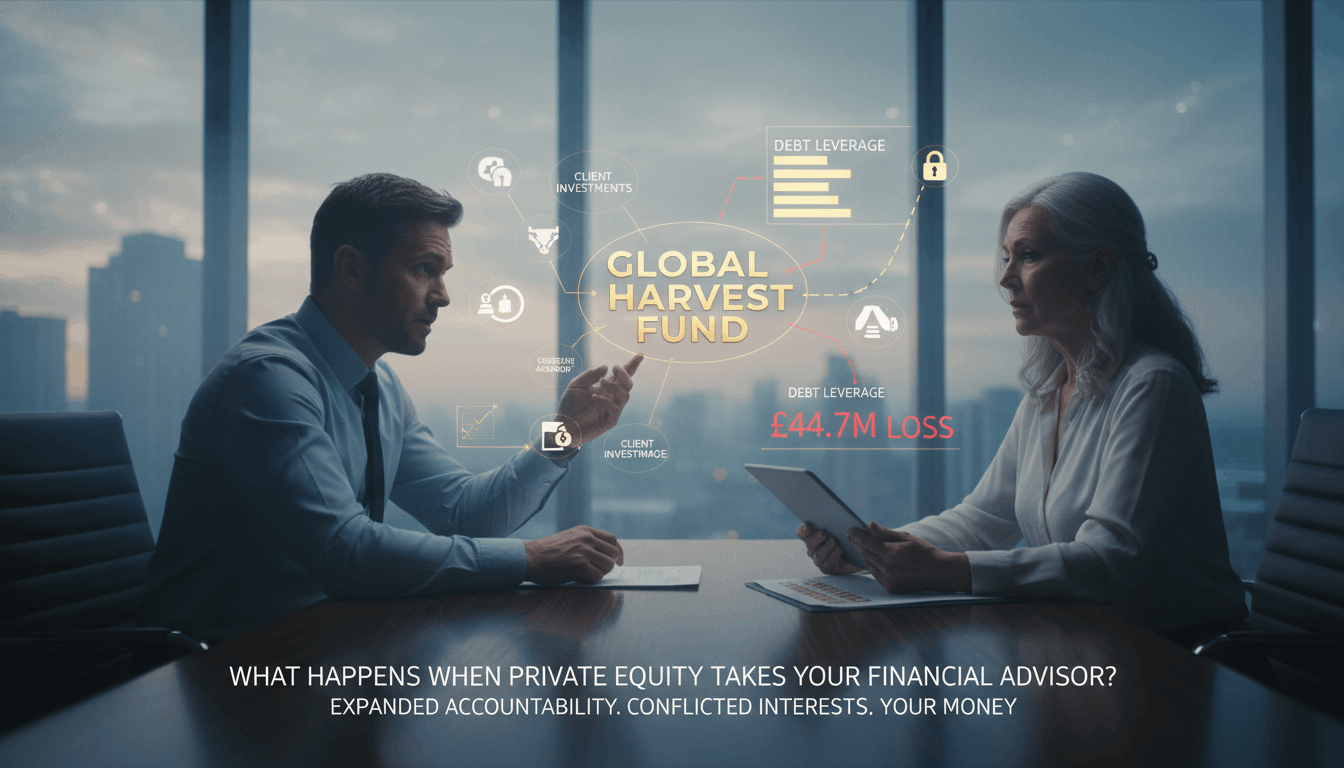

Debt levels and refinancing in major consolidators

One consolidator dominantly present in the UAE reported revenues of £77.4m, up 44 per cent, yet still recorded a pre-tax loss of £44.7m. Loan interest and amortisation, along with integration costs, consumed the revenue gains.

This issue isn't a theoretical balance sheet concern. High debt levels mean parent companies must generate cash to service loans. This situation creates pressure that affects how the firm delivers advice and which products it recommends.

How operating losses affect service quality

The advice firm keeps client investment assets separate from its balance sheet, and these assets carry regulatory protections. Your money isn't at direct risk if the parent company struggles with finances. But a parent company under financial pressure has less capacity to invest in service quality and more incentive to cut costs. There's also a structural temptation to prioritise group-level debt repayment over client outcomes.

The squeeze affects staffing levels and technology investments when private equity financial advisors operate under these conditions. It also limits the time advisers can spend with each client.

Regulatory reviews and client redress provisions

Provisions signal regulatory concerns about how private equity buying financial advisors has affected client treatment. The combination of high debt and operating losses creates a business model that is under strain, and regulatory redress further complicates it.

Questions to ask your financial adviser after a takeover

You hold more power than you might realise, but you need to ask direct questions to exercise it.

Who owns your adviser's firm and what's their investment horizon

Many clients don't know who owns their adviser's business. Global registers let you trace any regulated firm's ownership structure. The chain might lead to an offshore holding company or a private equity fund with no obvious UK or European presence. Ask your adviser to explain in simple terms who ends up owning the business and what their investment horizon looks like. A competent adviser will answer these questions without difficulty. Vagueness tells you something.

Are your investments in the parent company's funds

Your money might sit in the parent company's own funds. Request a written explanation of why those funds represent better value than a comparable low-cost index alternative. Most actively managed funds lag their measures over long periods on a cost and risk-adjusted basis.

Has your adviser's pay structure changed

Ask whether your adviser now earns more to recommend in-house products than external ones. That's a conflict worth understanding before you act on their next recommendation.

How to verify changes in writing

Get any post-acquisition changes to fees or service terms confirmed in writing. You might wonder whether your adviser's firm is truly independent.

Final Thoughts

Private equity takeovers create structural conflicts that may not serve your best interests. The move from independent advice to vertically integrated consolidators means your adviser faces pressure to recommend parent company products, whatever cheaper alternatives perform better.

Ask direct questions about ownership, compensation and product selection. You can protect your investments this way.

FAQs

Q1. How does private equity ownership change the way financial advisory firms operate?

Private equity takeovers shift advisory firms from independent practices to consolidated groups with vertically integrated structures. This means the same parent company often controls the advice, the investment platform, and the investment products themselves, capturing profit at multiple levels. The focus shifts from client-centred service to operational control and revenue generation across the entire value chain.

Q2. What conflicts of interest arise when private equity buys financial advisory businesses?

When private equity owns advisory firms, structural conflicts emerge because the parent company profits from both advisory fees and proprietary investment products. Advisers may face pressure—explicit or implicit—to recommend in-house funds over independent alternatives that might cost less or perform better. This creates tension between what serves client outcomes and what serves the consolidator's revenue targets.

Q3. Can clients leave if they're unhappy after private equity acquires their adviser's firm?

Yes, clients can leave a firm after a private equity takeover. However, the transition often happens gradually, and many clients do not immediately realise that the service quality has changed. Personal relationships and inertia make it difficult for clients to switch advisers, even when they should, which is why retention rates remain high even through ownership changes.

Q4. Why do financial advisers sell their practices to private equity firms?

Private equity firms typically pay premium valuations—often three to four times annual revenue—which significantly exceeds what advisers could receive through internal succession plans. Many advisers lack clearly defined succession strategies or pathways to partnership for younger team members, making the substantial payout from private equity an attractive exit option despite potential impacts on clients.

Q5. What financial pressures do private equity-backed advisory firms face?

Many large consolidators carry substantial debt from acquisitions and operate at a loss despite growing revenues. High debt levels create pressure to generate cash for loan servicing, which affects service quality, staffing levels, and product recommendations. Some firms have also set aside significant funds for client redress following regulatory reviews, indicating concerns about how ownership changes have affected client treatment.