Real Estate Diversification: Why Smart Investors Are Choosing Secured Loan Certificates Over Property

Real estate diversification has become a critical concern for investors tired of dealing with problem tenants, void periods, and shrinking net returns. Traditional buy-to-let properties once promised steady income, but the reality is constant maintenance calls and regulatory headaches while investors' capital stays locked away for years.

We're seeing a change toward alternative investment vehicles that offer real estate portfolio diversification without the operational burden. Secured loan certificates have emerged as a compelling option and provide fixed returns with quarterly income while eliminating tenant management.

This piece explores strategies for diversifying real estate investments and compares traditional property ownership against secured loan certificates. We'll get into real estate diversification benefits that include return profiles, risk mitigation features, and capital efficiency.

The Problems with Traditional Buy-to-Let Property Investment

Owning physical rental property sounds straightforward on paper, but the operational reality exposes investors to risks that fundamentally undermine portfolio performance. Understanding these friction points matters when evaluating options for diversifying real estate investments.

Tenant Management Headaches

Tenant-related issues create the most persistent drain on landlord returns. Renters who default on monthly payments trigger cash flow disruption right away. Some refuse to vacate when their tenancy ends and force property owners into lengthy legal eviction processes that rack up solicitor fees and court costs.

Property damage presents a recurring problem. A single irresponsible tenant can cause severe physical destruction requiring thousands in repairs. We've seen cases where simple roof damage costs €3,000 to fix and wipes out months of rental income. These aren't isolated incidents but predictable patterns landlords face over and over.

Low Net Returns After All Costs

The advertised rental yield rarely reflects what you keep. Management fees reduce your gross income right away. Maintenance expenses appear without warning. Void periods between tenants create income gaps while mortgage payments and bills continue. Insurance premiums and property taxes pile on with ongoing compliance costs.

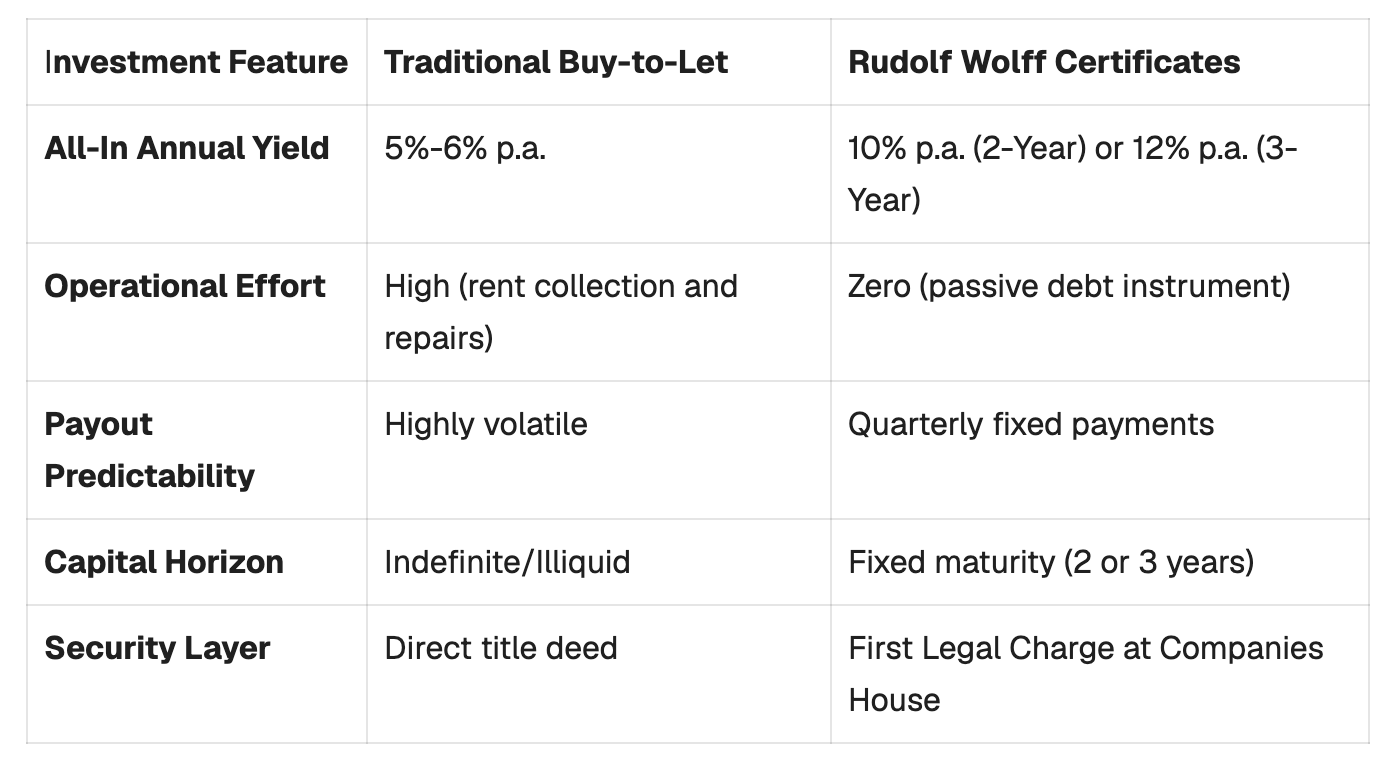

Factor in structural maintenance, property depreciation and legal fees, and traditional real estate yields just 5% to 6% per annum all-in, even when accounting for long-term capital appreciation. The real estate diversification benefits of buy-to-let investments become questionable then compared to passive alternatives.

Capital Illiquidity and Exit Challenges

Physical properties trap your capital for indefinite periods. The sales process can take months or even years to complete if you need urgent access to funds. You must find a buyer willing to pay your asking price, negotiate terms, complete surveys and work through legal conveyancing. Market conditions might force you to accept below-market offers just to access your own money.

Time-Intensive Property Maintenance

Ownership demands constant attention. Boilers break down. Plumbing fails. Electrical systems need inspection. Each issue requires scheduling contractors, getting quotes and overseeing repairs. This operational effort converts what should be passive income into an active, stressful commitment that absorbs your time without additional compensation.

What Are Secured Loan Certificates and How Do They Work

Secured loan certificates offer a structural alternative to direct property ownership. You subscribe to corporate debt instruments that deploy your capital into real estate development projects while eliminating operational responsibilities, rather than purchasing buildings and managing tenants.

Understanding the Simple Structure

RW Secured Lending Limited issues these certificates under a 150-year-old brand name. The company operates as an incorporated private limited company under UK law, with its registered office at 10 Orange Street, London, WC2H 7DQ. You can verify its legitimacy through the official UK Companies House Register using Company Number 17019488.

You're providing debt financing to the company, which then funds experienced developers. This makes you a lender rather than a landlord and fundamentally changes your position in the real estate investment diversification spectrum.

The Capital Deployment Process

Your pooled capital gets deployed as short-to-medium-term commercial loans to developers in the UK residential parks sector. These developers identify opportunities to convert campsites and holiday parks into luxury residential-style estates. The UK faces a housing shortfall and needs up to 500,000 new homes yearly but delivers less than half. Well over 3 million retirees seek to downsize, which creates urgent consumer demand.

Park homes average around £220,000 compared to a standard £470,000 detached UK home. This gives developers strong market pull. The build model uses modular units constructed off-site in factories with 10-year warranties. Development requires site preparation, roughly 6 months to construct, followed by a 6-to-12-month sales phase. This rapid lifecycle explains why RW Secured Lending typically receives full repayment within two years.

Fixed Return Mechanisms

The certificates offer contractual fixed yields: 10% per annum over a 2-year term or 12% per annum over a 3-year term. These returns arrive whatever the tenant behaviour, property market fluctuations, or maintenance emergencies. You receive your exact original capital back at maturity without benefiting from property appreciation, as the certificate is a fixed-income debt instrument.

Quarterly Payment Schedules

Payments arrive at the end of June, September, December, and March. You receive €6,250 every quarter from a €250,000 investment in the 2-year certificate, totalling €25,000 annually. No deductions for maintenance, agent fees, or tenant exposure reduce these payments.

Real Estate Investment Diversification: Comparing Returns and Risk Profiles

Numbers reveal the true cost of diversifying a real estate portfolio. A €250,000 allocation over two years exposes stark differences between traditional property and secured certificates when you analyse the data.

Side-by-Side Cash Flow Analysis

A €250,000 buy-to-let property targeting 5.5% all-in yield generates €13,750 gross each year. Hidden deductions erode this figure fast. One month of tenant default, a €3,000 roof repair, or broker fees when selling can slash real net gains by half or turn the year negative. Total 2-year real net returns range from €15,000 to €27,500 and come with intensive labour.

A €250,000 Rudolf Wolff 2-year certificate delivers a contractual 10% per annum, by contrast. Year 1 produces €25,000 in fixed cash flow, distributed as €6,250 across four quarterly payments. Year 2 repeats the same pattern. Operational deductions total €0. Total 2-year fixed net returns reach €50,000, paid on strict quarterly schedules to your account.

Operational Effort Requirements

Certificates eliminate tenant management. Buy-to-let properties need constant attention while certificates operate passively.

Capital Protection and Security Layers

The first legal charge protection registered at Companies House secures certificate holders. Investors verify protections through Company Number 17019488.

Market Exposure Differences

Certificates offer no asset appreciation. You receive the exact original capital at maturity and miss out on benefits from inflation in the property market. This trade-off delivers predictability over speculation.

International private placements and cross-border allocations require only specialised oversight. Expat Fiduciary streamlines compliance, onboarding and subscription frameworks. Your capital maps securely to verified asset pools. Contact Expat Fiduciary to request the detailed information memorandum or schedule a private consultation.

Real Estate Diversification Benefits: Security Features and Risk Mitigation

Multiple security layers distinguish secured loan certificates from traditional methods of diversifying real estate portfolios. These protections create structural safeguards that reduce investment risk.

First Legal Charge Protection

Your capital receives priority protection through First Legal Charge filings registered at the UK Companies House. You can verify this protection by visiting the official government-run register. Enter the company number 17019488 and navigate to the "Charges" sub-tab to inspect the active legal charges favouring institutional security trustees.

Developer Profit Margin Buffers

Developers funded through this model target a high 50% gross margin on each unit. This profit cushion provides strong interest coverage and ensures developers can absorb unexpected cost overruns or market downturns while clearing interest owed to certificate holders.

Transparent Corporate Structure

RW Secured Lending Limited operates as an incorporated private limited company with its registered office at 10 Orange Street, London, WC2H 7DQ. Unlike opaque offshore vehicles, you can audit the company's live legal standing.

Professional Oversight and Management

Paul Chadney manages the underwriting process. He brings over 25 years of experience from heading Barclays' lending team. Moore Kingston Smith serves as an accounting and financial advisor, while Faegre Drinker London handles legal structuring.

Regulatory Framework and Investor Protections

This promotion operates under UK Financial Services and Markets Act (FSMA) exemptions designed for high-net-worth or sophisticated investors. The certificates are unregulated alternative investment products where capital remains at risk.

Final Thoughts

Real estate portfolio diversification no longer requires direct property ownership, tenant headaches, or unpredictable yields. International private placements require specialist oversight.

Your capital maps to verified asset pools with proper compliance frameworks. Secured loan certificates deliver predictable quarterly income while you focus on what matters.

FAQs

Q1. What are the main types of real estate investments available to investors?

There are four primary types of real estate investments: residential properties (homes and apartments), commercial real estate (office buildings and retail spaces), industrial properties (warehouses and manufacturing facilities), and land. Each type offers distinct advantages and challenges that investors should evaluate based on their financial goals and risk tolerance.

Q2. How do secured loan certificates differ from traditional property investment?

Secured loan certificates allow you to invest in real estate development projects without owning physical property or managing tenants. You provide debt financing to developers and receive fixed quarterly returns (10-12% annually), while traditional property ownership requires hands-on management and tenant oversight and generates lower net returns (5-6% annually) after accounting for maintenance, void periods, and operational expenses.

Q3. What does it mean when a loan is secured by property?

When a loan is secured by property, the lender holds a legal claim (such as a title or deed) against that asset until the loan is fully repaid. This security mechanism protects the lender's investment by providing collateral that the lender can claim if the borrower defaults. In the case of secured loan certificates, First Legal Charge protection, registered at Companies House, provides priority protection for investors.

Q4. What are the key security features that protect secured loan certificate investors?

Investors benefit from multiple protection layers, including First Legal Charge filings registered at UK Companies House, developer profit margins of approximately 50% that provide substantial interest coverage, a transparent corporate structure with verifiable registration details, and professional oversight from experienced financial and legal advisors with decades of industry expertise.

Q5. Why do secured loan certificates offer higher returns than traditional buy-to-let properties?

Secured loan certificates eliminate all operational costs associated with property ownership—no tenant management, maintenance expenses, void periods, or agent fees. This allows the full contractual yield (10-12% annually) to reach investors through quarterly payments, whereas traditional buy-to-let properties face numerous deductions that reduce gross rental income to net returns of just 5-6% annually.