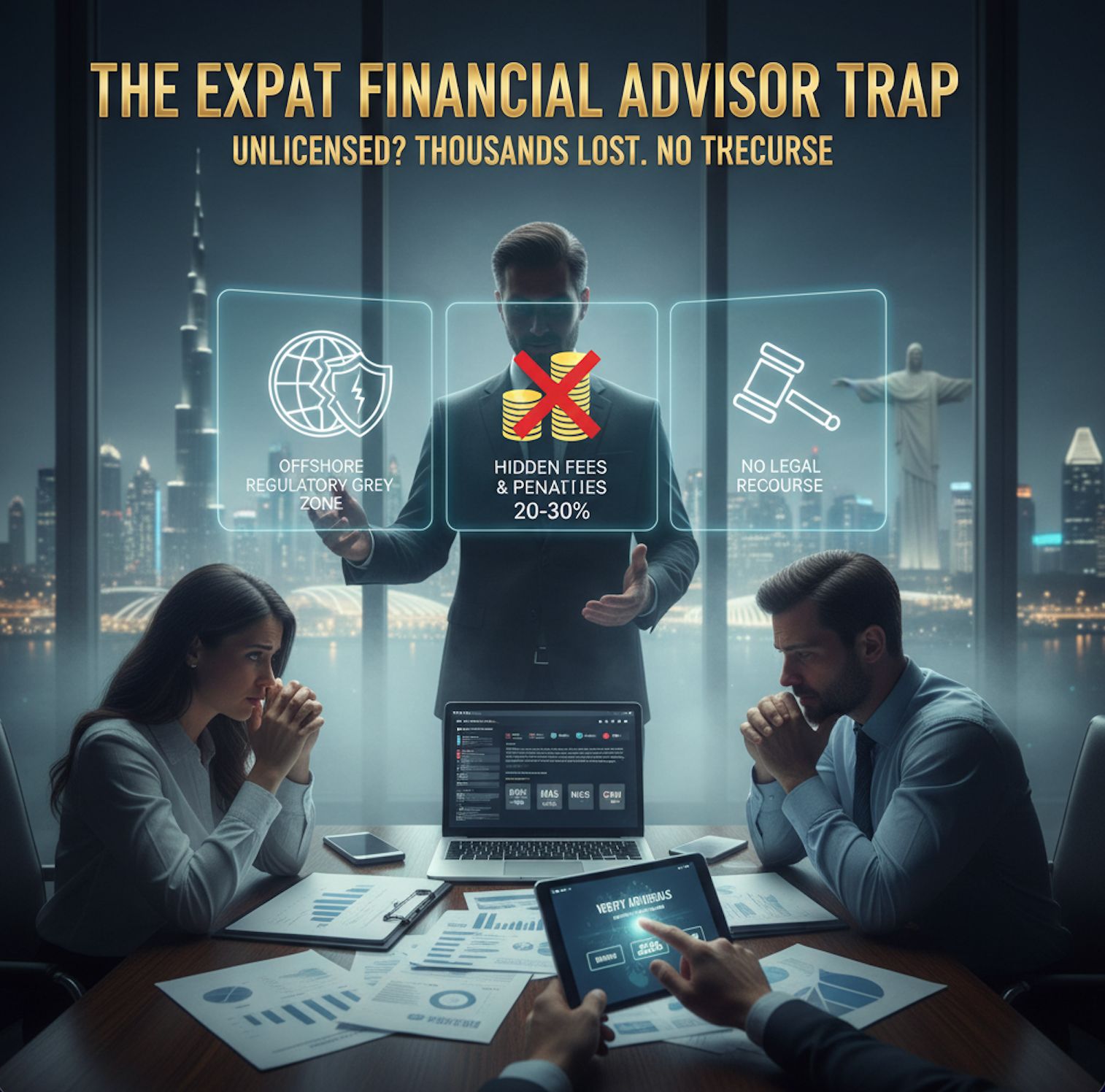

Expat Financial Advisor Licensing: The Hidden Truth That Could Cost You Thousands

Your expat financial advisor may be operating without proper licensing. You might never know until it's too late. Thousands of expatriates find this harsh reality only after facing financial losses with no legal recourse. The offshore financial industry operates in regulatory grey zones that leave you vulnerable to unlicensed practitioners.

This piece reveals what licensing actually means, how to verify credentials, and the true costs of working with unregulated advisors. You'll also learn how to identify the best expat financial advisor with legitimate licensing and fiduciary protections.

Why Expat Financial Advisor Licensing Matters More Than You Think

Local regulators in Dubai, Singapore, and Brazil exist for one purpose: to ensure anyone managing your money meets minimum standards of competence, maintains proper insurance, and operates with transparency. Offshore promoters structure their businesses to slip through the regulatory cracks of these jurisdictions and leave you exposed without the protections you assume exist.

The regulatory protection gap for expats

Regulators like the DFSA in Dubai, MAS in Singapore, and CVM in Brazil enforce strict rules to protect investors. These frameworks exist to prevent financial misconduct, verify advisor qualifications, and provide legal recourse when things go wrong. But expats face a unique vulnerability that domestic residents don't encounter.

You relocate to a new country and must guide yourself through unfamiliar financial infrastructure while building wealth in an environment where local regulations may not cover advisors operating from offshore jurisdictions. Promoters exploit this gap by targeting you through digital channels while maintaining their legal entities in light-touch offshore hubs like Mauritius, Vanuatu, or certain Caribbean islands. They appear professional, speak your language, and understand expat challenges. But they operate outside the regulatory framework designed to protect you.

The Gulf Cooperation Council countries present acute risks. Expat populations grow faster and often lack permanent roots. They are unfamiliar with local financial systems. Promoters exploit transitions between tax jurisdictions to pitch "tax-free offshore growth" that bypasses local regulatory oversight. Southeast Asia faces similar challenges, where promoters target expats from outside Singapore using digital channels and stay beyond the reach of local enforcement.

How unlicensed advisors slip through legal cracks

Offshore promoters use three main tactics to bypass regulatory requirements. They exploit the "reverse solicitation" loophole. Most jurisdictions prohibit soliciting financial business without a local licence. Promoters circumvent these restrictions by using their website as a passive magnet. You fill out a contact form on their website, which they use to claim they didn't target you inside the UAE or Singapore. They argue you travelled to their offshore jurisdiction. This is a legal fiction. The whole purpose of their search engine optimisation strategy is to target expats in specific countries.

Jurisdictional border-hopping allows them to evade enforcement. They set up legal entities in offshore hubs and target expats in regions like Saudi Arabia or Qatar. Local authorities attempt to investigate and find that you have no physical office, local bank accounts, or legal presence in your country.

They shield themselves behind the "financial media" loophole. These promoters claim their website provides "financial commentary" or "information" rather than regulated investment advice when confronted about their lack of investment licences. Behind closed doors, this generic commentary transitions into specific product placement and sales pitches naturally.

The actual cost of missing credentials

Working with an unlicensed expat financial advisor carries severe financial consequences. These promoters sell complex products where the provider pays them massive upfront commissions, often 5% to 7% of your total investment. Your lock-in period and surrender penalties fund this commission.

You attempt to exit the investment early and face penalties that can consume 20% to 30% of your capital. The promoter has already been paid and has no incentive to monitor your portfolio's performance or adjust your strategy as circumstances change. When things go wrong, you have no legal recourse. Without proper licensing, you cannot file complaints with local regulators or pursue claims through professional indemnity insurance.

A qualified expat financial advisor must comply with both the home country's and local jurisdiction's regulations. Promoters operating offshore ignore these requirements and leave you exposed to both financial losses and potential legal complications.

What Licensing Actually Means (And What It Doesn't)

Licensing confusion allows unlicensed operators to thrive in the expat financial space. Understanding what credentials mean separates legitimate advisors from offshore promoters who masquerade as regulated professionals.

Local regulatory requirements explained

Licensed advisors must meet specific standards that local regulatory bodies enforce. The DFSA requires minimum competence levels, professional indemnity insurance, and transparent operational standards for Dubai. Singapore's MAS enforces similar frameworks, while Brazil's CVM maintains strict investor protection protocols. These licences confirm that an advisor passed rigorous examinations, maintains ongoing compliance obligations, and operates under regulatory supervision with complaint mechanisms available to you.

Licensing creates legal accountability. It's not optional paperwork. Licensed advisors face audits, must segregate client assets, and risk losing their authorisation if they violate standards. This oversight structure protects your capital from misconduct that unregulated operators can commit with impunity.

The difference between offshore registration and local licensing

Offshore registration means a promoter registered a legal entity in a jurisdiction with minimal oversight. Mauritius, Vanuatu, and certain Caribbean islands allow company formation with light-touch regulation. This registration doesn't grant authority to provide financial advice in your country of residence.

Local licensing authorises an advisor to conduct financial business in a specific jurisdiction. A Singapore MAS licence permits advisory services there. A DFSA licence covers Dubai operations. Promoters exploit this difference by registering offshore while targeting expats in regulated markets through digital channels. They claim compliance through their offshore registration while avoiding the licensing requirements where you live.

Common licensing loopholes promoters exploit

Three tactics dominate the unlicensed promoter playbook. The reverse solicitation loophole operates when promoters position their website as a passive information source. You contact them by filling out a form. They argue that you travelled digitally to their jurisdiction rather than that they targeted you inside the UAE or Singapore. This argument is a legal fiction. Their entire SEO strategy exists to capture expats in specific countries, but structuring interactions as "reverse solicitation" attempts to circumvent local licensing rules.

This strategy creates enforcement dead zones when combined with jurisdictional border-hopping. Promoters establish entities in light-touch offshore hubs while targeting expats in highly regulated regions like Saudi Arabia or Qatar. Authorities identify a lack of physical presence, local accounts, and regulatory footprint in your country when they investigate.

The financial media loophole provides additional cover. Promoters claim they offer "educational content" or "financial commentary" rather than regulated advice when confronted about missing licenses. This commentary transitions into specific product recommendations and sales tactics behind closed doors.

Why your home country licence doesn't protect you abroad

A qualified US expat financial advisor must comply with both US and local jurisdiction regulations. Promoters ignore this dual requirement. Your advisor's home country credentials don't authorise cross-border advice. Regulatory protections from one country don't extend to transactions executed in another jurisdiction. You cannot pursue claims through your home regulator for advice received abroad from someone who does not have local authorisation.

How to Verify Your Advisor's Licensing Status

Verification protects you from financial disaster before you commit a single dollar. The best expat financial advisor welcomes scrutiny and provides documentation right away, while unlicensed promoters deflect these same questions.

Where to check licensing credentials by country

Each major expat hub maintains a public registry where you can verify advisor credentials. The DFSA website lists all authorised financial advisors operating in the DIFC in Dubai. Singapore's MAS maintains a complete register of licensed representatives and firms. Brazil's CVM provides searchable databases of registered investment advisors. Verify the advisor's name, licence number and authorisation scope with these regulators before any consultation.

This verification takes ten minutes but prevents years of financial complications. Request your advisor's specific licence number and regulatory body. Then confirm this information through the regulator's official website on your own, not through links the advisor provides.

Questions every expat should ask before signing

Ask where they are licensed. A legitimate advisor will state their specific regulatory authorisation right away. Ask who regulates their business and provides oversight. Request documentation of their professional indemnity insurance, which protects you if they make errors that get pricey. Confirm whether they operate under fiduciary duty or a suitability standard. The difference determines whether they must act in your best interest or recommend products that aren't obviously unsuitable.

Ask how they are compensated. Do they earn commissions from product providers, or do they charge transparent fees? What happens if you need to exit an investment early? These questions separate legitimate advisors from offshore promoters.

Red flags that indicate unlicensed operations

A real professional answers verification questions and provides documentation without hesitation. A promoter deflects, minimises or changes the subject. Watch for responses that redirect conversation toward product benefits rather than addressing licensing. Promoters claim their offshore registration is enough or reference vague "international credentials" without naming specific regulatory bodies.

Advisors who emphasise their website traffic, article volume or search rankings over regulatory compliance reveal their true business model. Digital visibility doesn't substitute for legal authorisation.

The reverse solicitation trick explained

This tactic deserves special attention due to its prevalence. Promoters structure their operation around claiming you contacted them first. They position their website as educational content, not active solicitation. Because you filled out a contact form, they argue you travelled to their offshore jurisdiction and bypassed local licensing requirements for soliciting business inside your country.

This is regulatory arbitrage that's worth considering. Their SEO strategy targets expats in Dubai, Singapore and other regulated markets. The passive website claim is a legal fiction designed to avoid accountability. Legitimate advisors don't rely on such loopholes. They maintain proper local licenses because they operate within regulatory frameworks designed to protect you.

The True Cost of Working With Unlicensed Advisors

Unlicensed promoters operate a business model that extracts maximum upfront value from your capital while minimising their ongoing obligations. The financial mechanics of this system favour the advisor at your expense.

Hidden commission structures revealed

Product providers pay unlicensed advisors massive upfront commissions ranging from 5% to 7% of your total investment. These payments happen the moment you sign and create immediate incentive misalignment. The promoter receives their compensation whether your portfolio grows, stagnates or declines. Their earnings are divorced from your financial outcomes.

These commission payments don't appear on your statements as explicit charges. The product structure itself embeds them, funded through the restrictions placed on your capital. The provider recoups this commission payout by locking your money into long-term contractual arrangements with severe exit penalties.

Lock-in penalties and surrender charges

Early exits from these investments trigger surrender charges consuming 20% to 30% of your capital. To name just one example, a $100,000 investment might incur $20,000 to $30,000 in penalties if you need liquidity within the first several years. These penalties exist to recoup the commission already paid to the promoter.

The surrender charge schedules span five to ten years and decrease as the provider recovers their upfront commission payout. Your capital remains trapped in an investment structure that may no longer suit your circumstances, meanwhile.

What happens when things go wrong

The promoter collected their commission at signing and has zero financial incentive to monitor your portfolio's performance. They won't adjust your strategy as markets move or your circumstances change. Their business model relies on high-volume client acquisition through digital channels, not ongoing portfolio management.

You discover the advisor has moved on to the next prospect when performance disappoints or your situation changes. Contractual savings plans and international insurance wrappers require active management that unlicensed promoters never provide after the sale.

Legal recourse: why you have none without proper licensing

You cannot file complaints with local regulators without proper licensing. Professional indemnity insurance doesn't cover unlicensed operations. Legal action faces jurisdictional dead ends when the promoter operates from an offshore entity with no physical presence in your country.

If you are holding offshore investments, international insurance wrappers or contractual savings plans set up by an offshore advisor, find what is happening beneath the surface.

Finding the Best Expat Financial Advisor With Proper Credentials

Finding the best expat financial advisor requires moving beyond digital content dominance to actual regulatory credentials and structural arrangements with your wealth goals. The difference between unlicensed promoters and legitimate advisors becomes clear when you get into specific markers.

Regulatory bodies in major expat hubs

Verify registration with the DFSA if you're in Dubai. Singapore advisors must hold MAS authorisation. Brazil requires CVM registration. These regulatory bodies maintain public registries where you can confirm an advisor's licence number, authorisation scope and compliance status. Legitimate advisors operate transparently within these frameworks because they have nothing to hide.

Fee-only vs commission-based licensing differences

The promoter relies on high-volume web traffic and operates without verifiable local licenses. They profit from opaque product commissions whatever your portfolio's performance. The fiduciary operates transparently and charges clear fee-only or performance-based fees. They maintain strict regulatory compliance and only succeed when your wealth grows.

Performance-fee-only models arrange advisor compensation with your portfolio's growth. When an advisor's success is tied to your returns, their incentives match yours. Commission-based structures create the opposite dynamic and reward product sales rather than portfolio performance.

What fiduciary duty really means

Fiduciary duty is a legal obligation to act in your best interest. This isn't a marketing claim but an enforceable standard. Advisors operating under a fiduciary duty must prioritise your financial outcomes over their own compensation. Suitability standards only require recommendations that aren't obviously unsuitable.

Documentation legitimate advisors provide upfront

Ask to obtain licence numbers and verify them with local regulators. Confirm professional indemnity insurance coverage. Request transparent fee structure documentation. A real professional provides these documents right away.

Do not mistake search engine dominance for professional competence. If you are holding offshore investments, international insurance wrappers or contractual savings plans set up by an offshore advisor, uncover what is happening beneath the surface. Contact Expat Fiduciary today to schedule a free, no-obligation review of your current financial structure. Our performance-fee-only model ties our success to your growth and provides the transparent protection your wealth deserves.

Final Thoughts

Your financial future depends on working with licensed advisors who operate under regulatory oversight. Unlicensed promoters cost expats thousands through hidden commissions, surrender penalties, and misaligned incentives that prioritise their profits over your portfolio's growth.

Verification takes minutes but prevents years of financial complications. Check regulatory registries in Dubai, Singapore or Brazil before signing anything. Ask questions about licensing, fees and fiduciary duty. Walk away if an advisor deflects or relies on digital visibility over credentials.

FAQs

Q1. What qualifications should I look for when choosing a financial advisor as an expat?

A financial advisor should hold recognised qualifications and be registered with the relevant regulatory authority in your country of residence. This includes licenses from bodies like the DFSA in Dubai, MAS in Singapore, or CVM in Brazil. They should also maintain professional indemnity insurance and be able to provide their licence number for verification. Look for advisors who operate under fiduciary duty, meaning they're legally obligated to act in your best interest rather than simply recommending suitable products.

Q2. How can I verify if my financial advisor is properly licensed?

You can verify an advisor's licensing status by checking the public registry maintained by your local regulatory body. In Dubai, check the DFSA website; in Singapore, use the MAS register; and in Brazil, consult the CVM database. Request your advisor's specific licence number and regulatory body, then independently confirm this information through the regulator's official website. This verification process takes only about ten minutes but can prevent significant financial complications.

Q3. What is the 80/20 rule in financial planning?

The 80/20 rule, also known as the Pareto Principle, suggests that 20% of your financial decisions drive 80% of your financial outcomes. In the context of working with financial advisors, this means focusing on the critical factors that truly matter—such as proper licensing, transparent fee structures, and fiduciary duty—rather than being distracted by marketing claims or digital visibility.

Q4. What are the risks of working with an unlicensed financial advisor?

Working with an unlicensed advisor exposes you to hidden commission structures of 5-7% of your investment, lock-in penalties of 20-30% if you exit early, and zero legal recourse when problems arise. Unlicensed advisors often operate from offshore jurisdictions to avoid regulatory oversight, leaving you without the ability to file complaints with local regulators or pursue claims through professional indemnity insurance. Their compensation is disconnected from your portfolio's performance, creating misaligned incentives.

Q5. What's the difference between fee-only and commission-based financial advisors?

Fee-only advisors charge transparent fees directly to you, and their compensation is often tied to your portfolio's performance, aligning their success with yours. Commission-based advisors earn money from product providers when they sell you financial products, typically receiving 5-7% upfront commissions regardless of how your investments perform. This commission-based structure can create conflicts of interest, as the advisor profits from product sales rather than your portfolio growth.